Truncation errors in PCFs

What are truncation errors?

Truncation error in conventional Product Carbon Footprints (PCF) is a serious problem that is overlooked far too often in carbon accounting. For many years it has been the largest elephant in the room of the carbon accounting industry.

At their best, emissions factors derived from PCF based on the Life Cycle Assessment (LCA) approach, can be far more specific than spend-based factors derived from an economic input-output model.

However, they suffer from the problem that supply chains are generally infinite and fractal in their nature. PCF analysis can only ever take account of a finite number of nodes in a supply chain. This means that PCF are always incomplete. The missing emissions and resulting underestimation of PCF is called a truncation error, and it varies in amount between different products, different industries and different countries.

It can be tempting to trivialise the problem, on the basis that PCF can include all the largest nodes. However they always miss out an infinite number of smaller nodes, whose cumulative significance is not intuitively obvious.

Truncation errors can vary between a few percent to over 50% of the total carbon footprint of a product.

Truncation error: The largest elephant in the room of the carbon accounting industry results from the inevitable truncation of supply chain pathways that occurs in all traditional life cycle analyses, because of the fractal nature of supply chains meaning that many of the smaller suppliers are missed from analysis.

How significant are truncation errors in Product Carbon Footprints?

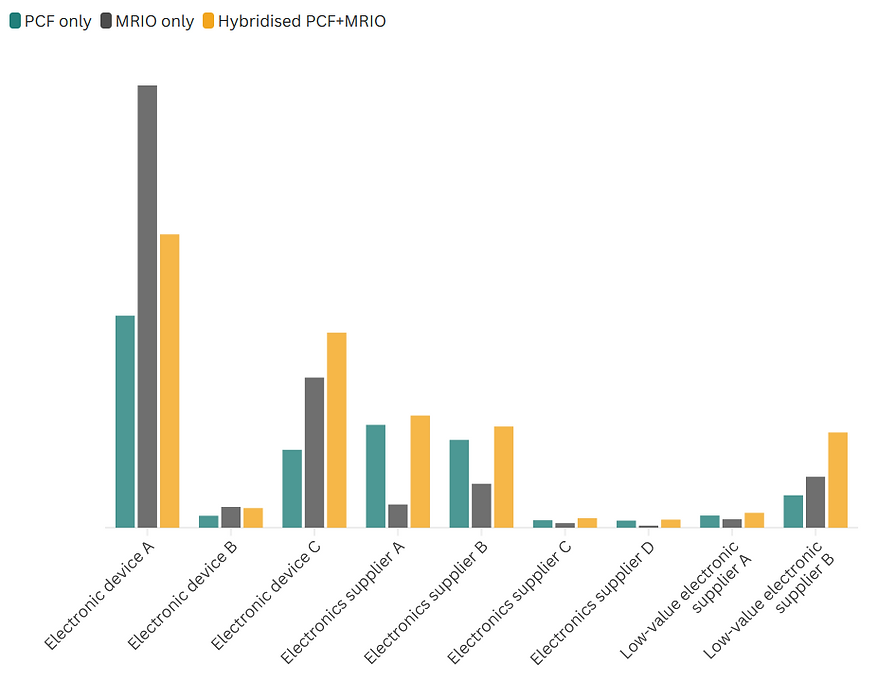

The graph below shows the difference between emissions calculated with PCF, spend-based data using an MRIO, and a hybridised PCF which removes the truncation errors, in a number of common electronic products. This data is from carbon analysis work by SWC for BT Group. Here we have anonymised the individual products.

For PCFs to be system-complete, making them them more reliable and compatible with spend-based emission factors, they need to be hybridised with input-output data to eliminate truncation errors.

Product and supplier emissions calculated with PCF, spend-based data using an MRIO, and a hybridised PCF. This data is from carbon analysis work by SWC for BT Group. Here we have anonymised the individual products and suppliers.

What is a hybridised Product Carbon Footprint?

A hybridised PCF is a PCF with the missing emissions from its truncation error replaced by the appropriate amount of spend-based emissions. The amount of adjustment needed is called a 'truncation error adjustment factor'.

Truncation error adjustment factors (TEAF)

You will need a truncation error adjustment factor (TEAF) for each PCF that you want to hybridise. Because assessments for PCFs include the same supply chain components, the parts they miss, the truncation errors are also the same for products within an industry sector in each country. This means that you can select the appropriate TEAF to use based on the industry sector and country of supply for your PCF.

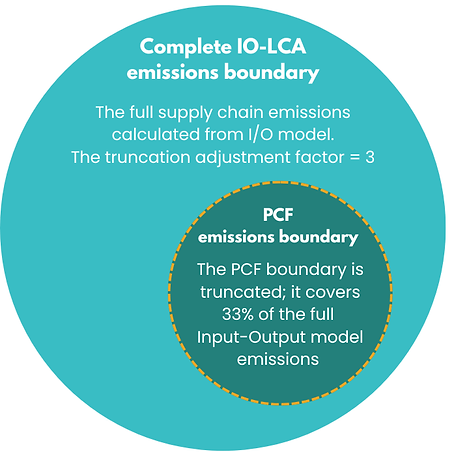

An example of a P-LCA analysis that shows it covers 33% of the full supply chain. The truncation error adjustment factor (TEAF) of 3 is therefore applied to create a hybridised P-LCA.

How do you create a hybridised Product Carbon Footprint?

-

Select your PCF derived emissions factors. These should, of course, be checked for their relevance, transparency, impartiality and methodological rigour.

-

Identify the industry sector to which the emissions factor relates, according to the classification taxonomy of spend-based factors used.

-

Where possible, identify the country to which the PCF relates. Often there will be an international component to the PCF, in which case, select a ‘best fit’ country.

-

Where possible, identify the following characteristics of the PCF methodology and how this compares with the overall methodology of the supply chain or product assessment that you are carrying out:

Inclusion or exclusion of emissions relating to capital infrastructure. If not known, use the default assumption that these emissions are excluded from the PCF.

Note that if you are using SWC MRIO, your assessment includes capital infrastructure.

Inclusion or exclusion of non-CO₂ climate impacts from aviation (such as contrails). If not known, use the default assumption that this is unaccounted for in the PCF.

Note that if you are using SWC MRIO, your assessment includes non-CO₂ aviation impacts.

Identify the significance cut-off criteria. (Default to 1% if not known.)

-

Select the relevant TEAF file based on the above methodological characteristics.

-

Multiply the PCF emissions factor by the TEAF for the relevant sector and country.

Your hybridised PCF is system-complete and can be used alongside spend-based emissions factors in your carbon assessment.

Total Carbon

Total Carbon gives you three datasets to enable you to use both spend-based and PCF emissions factors in one, system-complete, carbon assessment.

Using spend-based data (SWC MRIO), truncation error adjustment factors (SWC TEAF) and a set of trusted hybridised PCFs for the most common and high impacts products in Scope 3 analyses, you will get the most reliable Scope 3 carbon footprint.